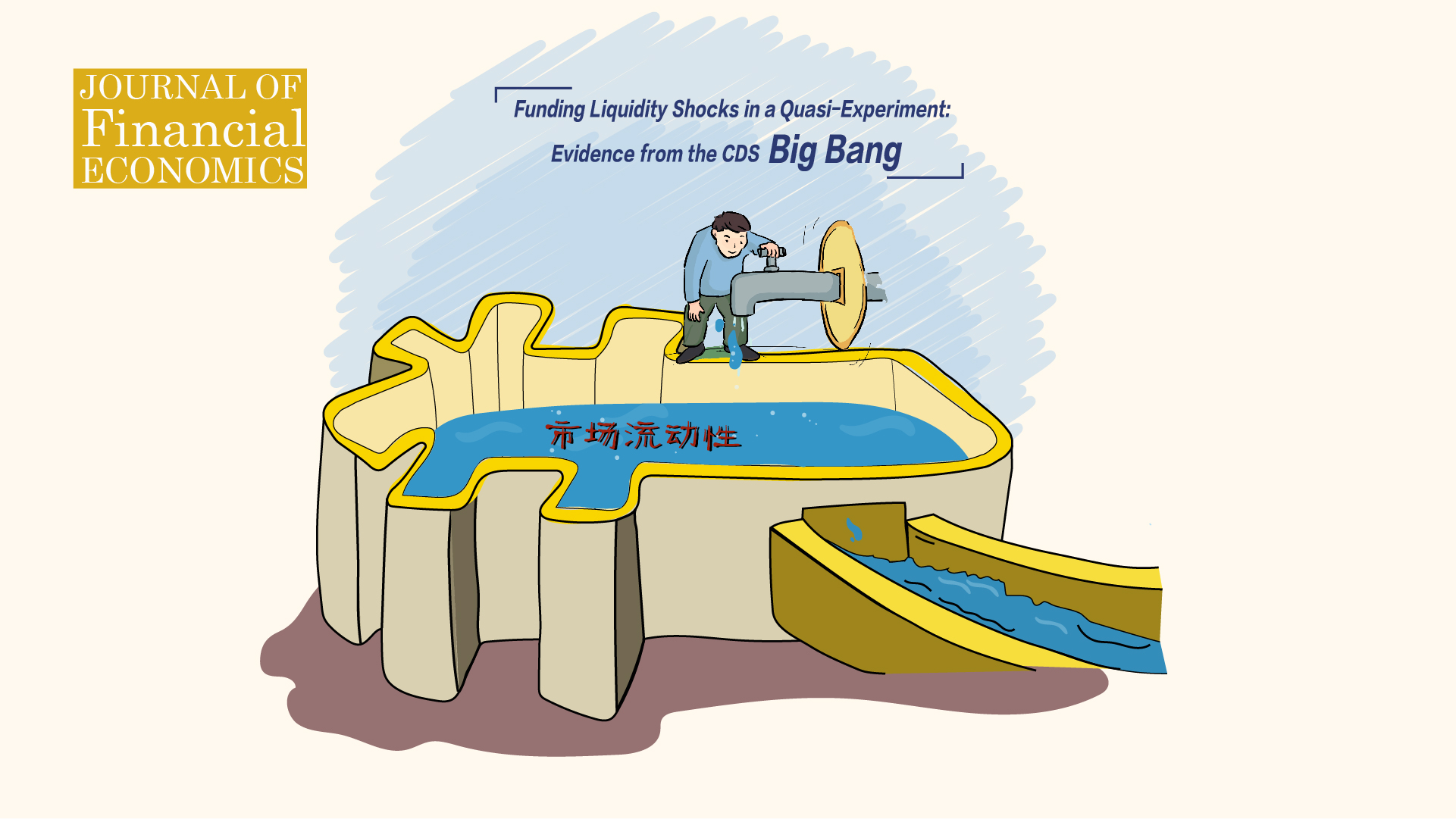

Recently, Assistant Professor Xinjie Wang from the Department of Finance at the Southern University of Science and Technology (SUSTech) has published his research article “Funding Liquidity Shocks in a Quasi-Experiment: Evidence from the CDS Big Bang” in the Journal of Financial Economics (JFE), one of the top journals covering financial economics. The article is co-authored with Professor Yangru Wu and Ken Zhong from Rutgers University and Professor Hongjun Yan from DePaul University.

Intuitively, a funding shock for market participants impairs their ability to trade, which leads to a fall in market liquidity and pushes prices away from fundamentals. As market liquidity dries up, margin requirements could also rise and exacerbate existing losses, resulting in a liquidity spiral. Identifying a causal relationship between funding liquidity and market liquidity is challenging because exogenous shocks to funding liquidity are rather rare. The goal of this paper is to test whether a causal link between funding liquidity and market liquidity exists empirically.

This paper uses the advent of the standardized fixed coupons for trading credit default swap (CDS) in April 2009, the so-called CDS Big Bang, as a shock to funding requirements of trading CDS contracts and then trace out its ensuing impact on market liquidity. Before the Big Bang, buyers of CDS protection paid sellers a fair-value spread such that the net present value (NPV) of the contract was zero at the start of the contract.

Therefore, aside from any initial margins, trading CDS required no upfront capital from either buyers or sellers. However, after the Big Bang, buyers of CDS protection pay sellers a chosen fixed coupon, e.g., 100 or 500 basis points (bps), instead of the fair-value spread. To compensate for the difference between the fair-value spread and the chosen standard coupon rate, an additional upfront payment is exchanged between buyers and sellers to make the NPV of the contract equal to zero at inception.

While CDS bid-ask spreads decline in aggregate after the Big Bang, they do so less for contracts that require larger fees. Furthermore, the funding effect is stronger for smaller and riskier firms and non-centrally cleared contracts. The effect also becomes stronger after Deutsche Bank’s exit.

Assistant Professor Xinjie Wang of the Department of Finance at SUSTech is the first author. Associate Professor Ken Zhong of Rutgers University is the corresponding author of this paper. This work was supported by the Southern University of Science and Technology under the Startup Grant.

Article link: https://doi.org/10.1016/j.jfineco.2020.08.004

Xinjie Wang’s website link: http://faculty.sustech.edu.cn/xinjie.wang/

Proofread ByAdrian Cremin, Yingying XIA

Photo By